Understanding Boost Sales with In-House Financing

In the current competitive sales landscape, retailers and service providers are continually trying to identify new means of eliminating friction during the purchase process and conquering larger numbers of conversions. Of the strategies that are there in the market, home financing has become one of the strongest methods to be used to enhance the deal closing rates. Rather than counting on third-party funding sources or forcing the customer to decide to either pay the entire sum immediately or struggle with choices, companies that use direct financing to customers provide a chance to a larger number of individuals to respond in the affirmative, although financial limitations could mean otherwise. The in-house financing knowledge brings a shift in the dynamics of the sales transaction in that affordability issues are resolved, easier approvals and better relationship with the customer which in the end translates to higher close rates.

The idea is simple in that when the customer feels that he is able to afford the product or service without straining his financial status, he is most likely to gain a purchasing decision faster. This is not only an issue of convenience, but rather of establishing a sales atmosphere where the perceived entry barrier is considerably lessened. Whether the retailer is ready to sell furniture on monthly deferred payments or a car dealer willing to offer a loan in-house financing, or a medical service care provider offering the staged payment, having an option of an advanced in-house financing program changes the discussion regarding the products and services offered by the company, which now shifts to, how can I make it work? Such a cognitive change can prove to be the tipping point towards making more transactions.

The Direct Link Between Financing Options and Closing Rates

Among the most significant considerations provided by in-house financing in their ability to increase deal closing rates is the fact that they affect the decision making behaviour of customers directly. In most instances customers enter a shop or come to a service provider interested in a product yet doubtful of the ability to be able to afford it. Failure to access financing through an external bank, having to have long periods of approval, or financing terms that are rigid may just drive them away. By funding from within, such delays and uncertainties are eliminated. Approvals are usually quicker, the requirements are apt to be flexible and even payment schedules can be set down to the budget of the customer. This forms a smooth transition between being enticed and buying.

Psychologically, the existence of financing in house changes the perception of risk on the side of the customer. They are not agreeing to a huge upfront payment, instead they are agreeing to small affordable payments which are predictable. The game of sales has changed in this way. Instead of justifying the cost, sales professionals would be able to concentrate on value and virtues. A salesperson will be able to talk confidently on how a quality product can be acquired by paying a manageable fee monthly and thus the product appears to be affordable. The customer is empowered and the fear of paying lump sum payment is removed and better purchase decisions are made.

Statistically speaking, companies with in-house financing often record a vastly improved closing ratio. This is not only due to the fact that larger numbers of customers can meet the credit requirement when the credit requirement is internalized but also because customers feel good by the trust and convenience given to them by the retailer. They are interacting with the business with whom they can ultimately develop goodwill and thus objections at the course of the sales process can be limited because they feel as though they are not communicating with an abstract financial institution.

Removing the “Price Shock” Barrier

The sticker price is one of the primary factors that would make potential customers withdraw their purchase. Even when they find the product or service to be desirable or intended they may not have the strength to conceive themselves affording the whole amount in one go. This is referred to as price shock and it is a sales killer in any industry. The in-house financing offers a sophisticated approach redefining the discussion in terms of affordability instead of the amount of total cost. The lowering of the purchase cost to monthly, bi-weekly or other installments suffices to change the mindset to whether or not the small payment amount can be accommodated in the customers budget.

This change is especially significant on the high-ticket items. This is the case in industries such as the home improvement industry, automotive industry, medical procedures, and luxury goods where a great number of customers do want but do not necessarily have the immediate capital. When the company is able to say, with certainty, as, “We can work this out with you with flexible payments,” then the sale is maintained. The customer will not be compelled to leave before making the decision after obtaining funding in other sources, a process which mostly leads to lost sales to the competitor. Rather, the customer is able to make a decision there and then, and this ensures that there is a higher probability of closing the deal.

Creative pricing can also be done through in house financing where the pricing can be to the needs of customers. As an illustration, a retailer can give the buyer a couple of months of zero interest period, or make the first payment later, to help the buyer with breathing space. Such terms and conditions can be customized to meet the risk appetite of the business but still provide the customers with a fine motivation to complete the sale. Hesitation disappears and decision-making hastens as long as a payment plan seems possible and reasonable.

Building Trust and Long-Term Relationships

Closing goes beyond getting one deal, it is also about building a relationship that can bring repeated deals and referrals. The role of in-house financing is special in this context since it makes the business a companion in the monetary life of the client than the seller in business. When a firm finances individuals directly, this is an indication that the company is ready to collaborate with its customers in order to satisfy the requirements. Such person-to-person interaction can usually result in increased customer satisfaction, which may be translated into loyalty.

This will make customers feel assisted in making a purchase and chances are higher that they will come back with future needs. They will also tend to refer the business to their friends and relatives. The recommendations made by word-of-mouth are valued highly and a company that is recognized to have made the purchases affordable can develop a very strong reputation within its neighborhood. This reputation also contributes to increased closing rates as the new customers are already anticipating a good and conducive experience.

Also, having the financing relationship within the company ensures that the business has more control on its customer relations. The business may communicate directly with the customer, organise payment terms and sort any problems out instead of handing them on to a third party lender. The type of control will enable more effective service recovery in case of any issues and give more chances to sell on upsell or cross-sell within the financing period.

Competitive Advantage in a Crowded Market

The competitiveness of the industry is such that, sometimes, the speed at which deals are closed may spell the difference between profitable existence and survival. Having in house financing may be an effective differentiator. Flexible financing can be used as one of the factors that lead to a customer purchasing a product when they have one at multiple options. Although one competitor may provide the same product/service at a similar price, one that can offer that finance easily and within reach may prevail.

Businesses are also able to adjust their offers to suit the precise requirement in the market through in house financing. As an illustration, during economic bad times when consumers are less willing to spend, the low-interest or deferred-payment selling solutions may stimulate the sale. Promotional financing like holidays discounts on top of convenient terms of payment may incur a sense of urgency and oblige customers to buy at the time.

In the case of niche or specialty items, in-house financing can increase the number of customers who are able to purchase the item by getting them at a level that people may have felt most individuals could not afford. Not only will this increase the volume of sales but it may improve brand perception as well. The strategic advantage of being viewed as a flexible company with a customer-centric approach that is hard to replicate by the competitors who may lack a source of external financing partners is enjoyed by the company in question.

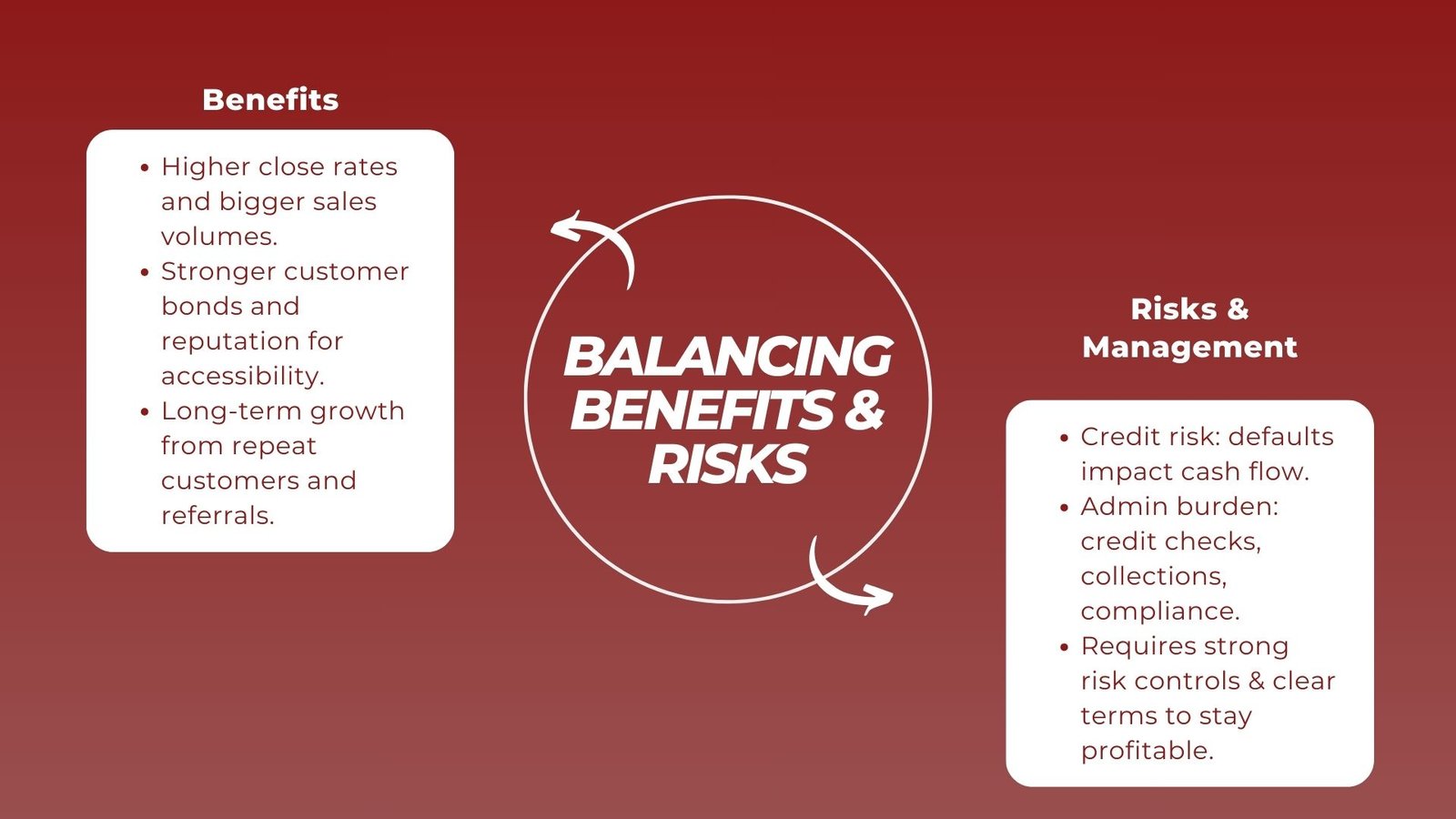

Financial Considerations and Risk Management

Although the benefits of in-house financing in increasing the rates at which deals are closed are quite evident, there are financial implications that should be treated with caution by the business. By giving credit to customers, one is exposing himself to certain amount of risk. Unpaid or delayed accounts can affect the cash flow and even profitability unless properly taken into account. But through careful planning all these risks can be eliminated and the benefits of the increased sales are still enjoyed.

Companies which provide in-house financing services require well-developed credit assessment, payment monitoring and collection systems. Although approval mechanisms may be less strict than those used by the conventional credit institutions, there must be evident rules of assessing whether a customer would be in a position to repay. The open terms and clear communication are also crucial to prevent misunderstandings and to make customers explicit of their duties.

It is of prime importance to structure funding conditions that can both attract the customers and manage the risk. The interest rates, charges, and repayment terms must be established to cover the administrative expenses that may also incur losses without being exorbitant on the customers. Most companies have ideally succeeded when their smaller financing programs are properly monitored on repayment performance to build their way up after finding the best ways to streamline their operations.

The financial course benefits for professionals in terms of increased closing of deals, when properly managed, is usually more than the expenses and risks involved in undertaking an in-house financing. An increase in the closes will result in revenue and the goodwill created by flexible payment options can translate into long-term profitability through repeat business and referrals.

Conclusion: Turning Flexibility into Sales Success

In-house financing is not a mere payment option-it is a sales tool that can directly affect the rate of closing deals. With less price shock, faster approval time and development of trust, companies can easily turn qualified leads into paying customers. The capability to deliver a resounding yes to more customers in time can ensure the continuous flow of the sales pipeline and bind the contacts that can result in long lasting loyalty.

Many customers may have an infinite number of options in such a market, and sales possibilities may be easily lost, so in-house financing may serve as the pivotal point. It enables customers, improves competitiveness and develops a reputation of accessibility and service. Although it must be properly managed so that the risk is not too high and the reward too low, in-house financing can be an extreme growth tool because the possible reward of more closing rates and customer satisfaction is quite founder-friendly. The trend, when used properly in businesses, will lead not only to increasing the number of signed deals but also enhancing its standing in the market long after the year has changed.