Understanding In-House Financing Explained

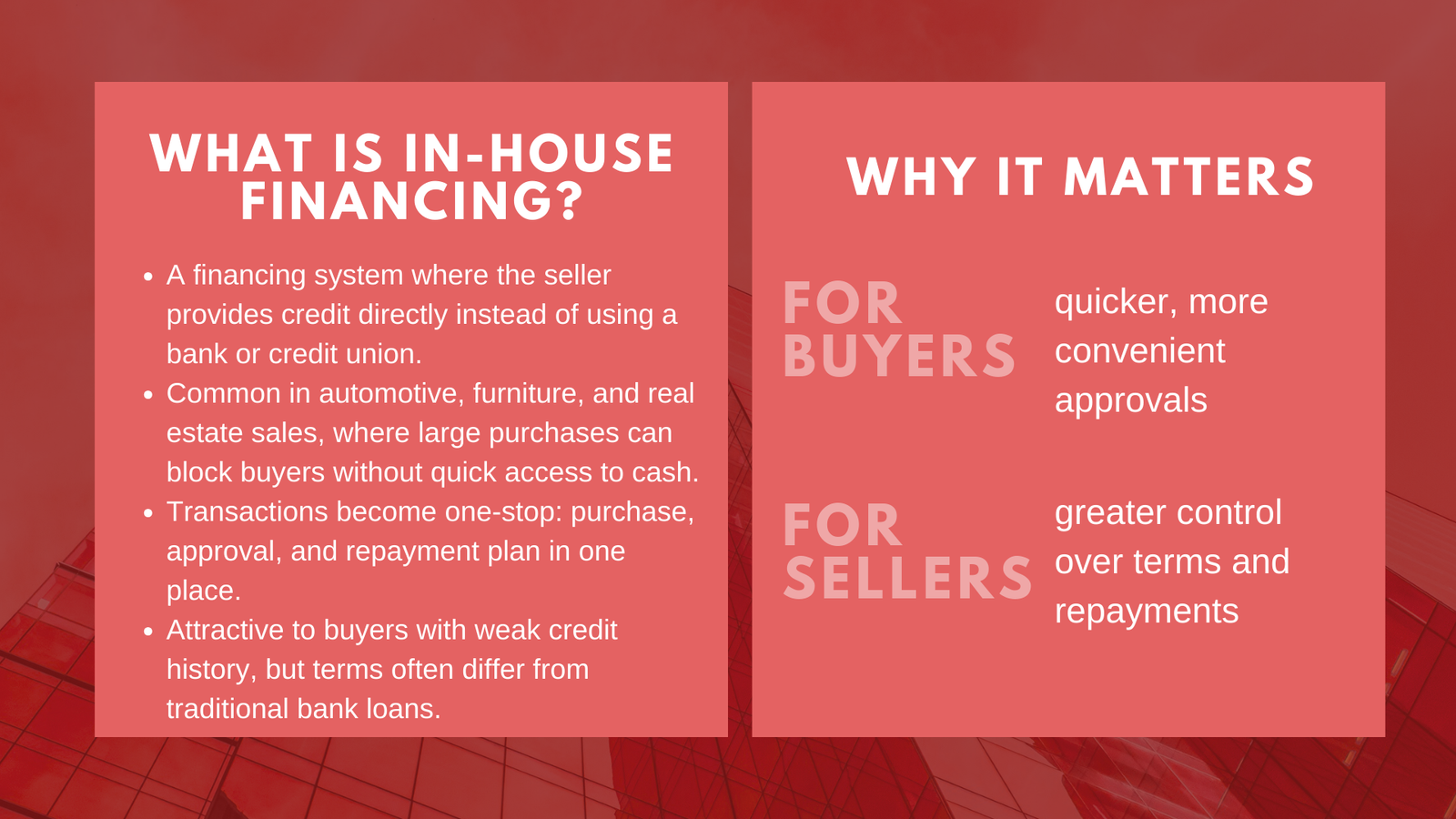

In-house financing is a financing system where an organization provides its credit or payment program directly to bodies as compared to a third-party lender e.g. bank or credit union. The model is commonly employed in the automotive sales, furniture selling, and real estate business in which a massive purchase might be an obstruction to customers who may lack quick access to cash or other funds to qualify before receiving conventional financing. The seller even has more oversight of the financing terms, approval of the funds given and the structure of repayments since there is no third party lending institution to rely on. In case of buyers, in-house financing may offer a quicker and more convenient means of finalizing a transaction, albeit with certain factors that must be realized prior to signing some papers.

The attractiveness of the in-house funding method is in its ease and concept. This usually occurs all through the sales transaction in the sense that the customers are able to make a purchase, get approved and make payment plans in a single location. This may be particularly appealing to those buyers whose credit history is less than stellar, when housing finance companies will be more likely to be able to entertain other qualifying benchmarks. Interest rates and repayment terms might however vary widely with the interest rates and the terms of normal loans since the seller is acting as a lender. It is important to understand how in-house financing is possible, the advantages and risks associated with it to aid both consumers and business owners to make their judgments. For individuals looking to deepen their knowledge of financial systems, options such as Professional finance certification courses Singapore can provide useful insights. Similarly, businesses that want to strengthen employee skills may consider Industry-specific in-house training solutions Singapore to improve financial decision-making within their teams.

How In-House Financing Works

The mechanics of financing in-house itself is fairly simple. The business gives credit to customers rather than sending them to lend money through a bank or credit provider; the business takes up the repayment of the loan instead. Considering the automotive sector, the example is the buy here, pay here, dealerships where customers can choose a vehicle, negotiate a price and make payment arrangements under the same roof. Dealerships do not sell the loan to a third-party lender, but instead they keep the debt and receive payments during an agreed duration of time.

This prevents having to meet certain limits of the lending terms that the banks have in terms of credit score or heavy income documentation. Rather, decisions about approvals may be made on an aggregate with respect to employment, income levels, and size of a down payment. The seller sets the terms of financing including interest rate, duration of paying, and installment. The payments are usually made to the business directly- either at an office, through the post or on an electronic device.

As far as the seller is concerned, providing in-house financing creates extra workload, i.e. the seller will be assuming the role of assessing borrowers risk, collecting repayments and providing services in a case where the borrower may default. This implies that necessary systems should be established in the business to evaluate the credit and recover the debt and also maintain capital to cover the event of non payment of balances. The seller on the other hand is able to generate more revenue in terms of interest and even sell more due to easy access of the products by more customers.

Benefits for Buyers

Accessibility is a benefit of in-house financing to the buyers. The customers who have been rejected by the traditional loans because of low credit scores, lack of credit history or unusual salary/income might realise that in-house financing can provide them an opportunity to purchase items that otherwise they would not be able to afford. The sellers can put more weight on the current financial capability of a buyer over and above past credit problems thus easier approval.

Convenience is another main advantage. Under in-house financing, the buyer is normally able to do the whole transaction in the same place without having to submit numerous applications and wait a long time before the bank approves the loan. This may be especially attractive when the purchase must be made in a time-sensitive manner, such as when an automobile has to perform duties of commuting to work.

In-house financing in other instances, is more flexible in structuring the terms of pay. The sellers can be willing to restructure repayment terms to fit a borrower to his or her payday or unable to make penalty-free repayment in advance. Although the interest rate might be high compared to that applied by banks, the convenience of easy entry and quick processing might be of bigger value to the buyers depending on the value of having easier purchasing power.

Benefits for Businesses

It can be an effective method of sale since businesses may be able to give in-house financing. Elimination of the use of third-party lenders would allow the companies to increase their target group of customers as well as those who would otherwise fail to access the market. The expanded customer base has the potential of resulting in a higher volume of sales especially in an industry where the cost of making initial large investments happens to be a typical drawback. For those in the finance sector, gaining Professional business valuation skills in Singapore can also support better decision-making when implementing in-house financing strategies.

Businesses can also use in-house financing to create closer relationships with customers. By engaging in both the sale and financing, a company is able to keep contact with customers to continue with the repayments. Such relationships may promote brand loyalty and create possibilities of repeat revenue. Also the interest taken on financed sales is another source of revenue other than profit generated during initial sale.

The second benefit is that one gets to regulate the terms of funding and tailor it to suit business objectives. An example would be that a retailer may offer promotional financing, at a low or no interest rate to a certain time frame to encourage customers during a low selling season. Likewise, a dealership could offer longer-term payments on the products of high prices and thus the probability of upselling enhances.

Risks and Considerations

Although the advantages of in-house financing are very apparent, there are risks that should be taken into consideration by both buyers and sellers in case of in-house financing. The cost is probably the greatest disadvantage to the buyers. The increased risk of loaning to customers who may not traditionally find themselves in a financial position to secure a loan typically results in a seller mitigating the risk by increasing the interest rates associated with the loan to customers. This may end up costing quite a lot over the life of the loan as opposed to bank funding.

It is also important that buyers note that in-house financing flows might carry more severe implications on late payments. Because the seller retains the loan personally, the possibility of default allows a quick repossession of the product, be it a vehicle or equipment, without the drawn out legal procedures involved in a bank foreclosure. This is attributed to the fact that buyers ought to exercise thorough scrutiny of the repayments and warrant that they should be in a good position to exercise the payments on a continuous basis.

On the part of the seller, the threat of non-payment is the main one. Companies that provide in-house finance should be ready to deal with delinquencies and defaults, which may be resource-draining and can affect the cash flow. It also involves the administrative overheads of operating an internal credit and collections operation which could necessitate the need to employ more staff, educate them and gain legal expertise.

Is In-House Financing the Right Choice?

Choosing in-house financing or not is a matter of circumstances. As to buyers, the decision must be made with references to their finances, credit rating and possibility to obtain traditional financing. Relative to lower interest rates on bank loans, higher interest on loans would only be more economical to those that are able to qualify bank loans at lower costs. But with some buyers that require quick credit decisioning, may have credit issues, or just want the convenience of a single point transaction, in-house financing may be an effective option.

In-house financing by businesses is a strategic option that can enable one to sell more goods and grow customers bases, but it should be carefully planned and risk-managed as it has pitfalls. The companies must make sure they have enough monetary cushions to meet possible defaults and powerful mechanisms to assess and track the risk of borrowers. Moreover, open sharing of terms of funding is also essential as it creates a level of trust and eliminates cross purposes.

Properly used, in-house financing is a win-win scenario, in which customers are able to gain the access to needed products, whereas businesses could increase revenue and market the way. Both parties however must enter into the deal with their eyes open in regard to what the demands, the cost, and the dangers that might be involved with the contracts. By this means, in-house financing may become a useful means of increasing purchase potentials and creating long-term customer relations, not to mention the balance between frugalness and availability here.