Understanding In-House Financing for Retailers

Retailers have now turned in-house financing as a business strategy in order to increase customer loyalty, sales conversions, and generation of secondary revenue streams. In contrast to conventional bank lending or credit programs to third parties, in-house financing is done by the retailer to the customer and usually on a high-value item or service concept. It is the type of model whereby retailers negotiate their own terms as the lender, interest rates and loan repayment schedules. Lately, it has gained popularity in other businesses such as furniture, electronics, appliances, and even in selling cars where factors such as the chance to pay the money at a later date can change a person’s decision whether or not to purchase an item. Knowledge of mechanics, advantages and disadvantages of in-house financing are very important to the retailer considering this method because it encompasses aspects of sales strategy, financing, and even customer relationship building. Insights similar to the Power of tailored in-house training Singapore demonstrate how customization can strengthen strategies and improve outcomes.

What In-House Financing Really Means

Fundamentally, in-house financing is a credit facility wherein the retailer performs all the operations without the need of an outside funding institution. Practically, this would imply the customer seeking financing in-store, the store would run a credit-check on the customer, and in the event of credit being given the customer would enter a payment arrangement with the store itself. Depending on the target market, the retailer can do credit checks or adopt other ways of evaluating risk. To lure away potential customers who may not qualify through the mainstream borrowing avenues, in some contexts, the in-house financing is advertised as canvassing no credit check or easy approvals.

This structure may vary in form. In certain businesses all the financing is done internally where the retailer assumes all the credit risk. In another format, the retailer ties up with a financing company and yet markets the offer under the label of in-house with itself being the first point of contact to the customer. On the one hand, the benefit to a retailer is the possibility to adjust the terms to the purposes of the business and the requirements of the customers. Terms allowing payment to be split over time, the amount of down payment required, paying interest, and special deals on the interest that may be obtained like interest-free terms can all be varied to suit the market and what the customers demand.

In-House Financing to sell products is not an objective to many retailers as it is a competitive factor. In cases where other sellers may necessitate upfront payment, or third-party financing consent, the facility to offer financing at a direct level may become a determining factor by the customer who is faced with numerous choices.

Why Retailers Offer In-House Financing

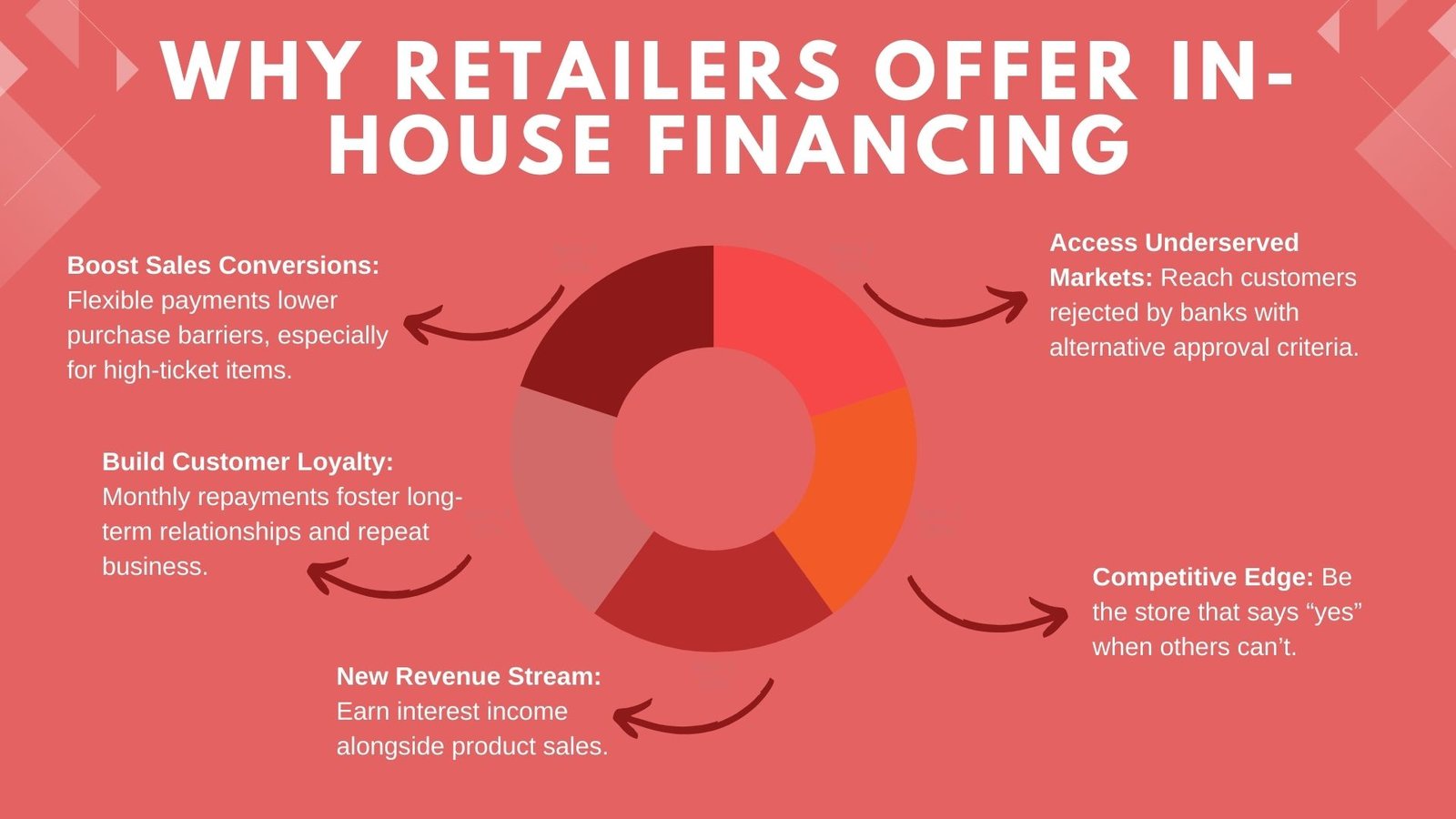

Retailers resort to in-house financing due to a number of considerations and the most evident is growth in sales. The customers usually have low budget constraints or may be reluctant to spend lots of money at once. Retailers provide flexible payment options; therefore, the financial aspect of the purchase barrier is lowered. This is significant particularly in industries with high end products which may be highly priced with the long term value like domestic appliances, jewelry or medical devices. The payment flexibility, i.e. offering to pay not now but in the future, has a chance of converting an indecisive shopper to a paying one.

The in-house finance contributes to customer loyalty as well. The stores where the customers finance directly are opinions that stay long after purchasing the original product or commodity. The monthly payments foster a continuous relationship and in case the experience is favorable, the customer is more likely to repeat in the future. Such retention effects may prove to be particularly useful in competitive markets.

Furthermore, financing presents the chance of retailers to gain their interest income besides sales. Although competitive interest rates have to be provided to stay attractive, the interest accrued over time may be an important secondary source of profit. In this manner, financing can be used as a symbol of sales and a source of revenues in the form of a financial product.

The other reason why retailers adopt in-house financing is because they can serve underserved markets. There are a great number of consumers who cannot receive traditional financing in the banks because of poor credit history or previous monetary setbacks. Retailers are able to offer credit to such customers by establishing their own criteria of approval to increase their market base. Although this entails more credit risk it could lead to increased customer loyalty by customers who appreciate the potential of having finance at a time when other sources are not open.

The Mechanics of In-House Financing

Advanced In-house financing is the process that usually begins with the application that can be filled either online or in-store. The retailer will then review the application made by the customer, which may entail credit scores, verifying earnings or general credit risk assessment techniques. Some retailers have very automated approval processes so some decisions may be made near instantly, whereas other retailers can require manual review especially on higher credit amounts.

Upon the approval, the retailer and the customer are agreeing on the financing conditions. This will be the amount of loan, interest rate, period of repayment and special promos. There are in-house financing programs to interest free payment programs of payment deferral or early pay discount. Such promotion words may be very compelling sale stimuli particularly when they align with seasons on sale or on launching a product.

Payments are usually received monthly and the retailer has to do the administrative work and operations of maintaining a balance, receive the payments and follow up the late accounts. Technology can be very important in this aspect, where point-of-sale and finance management softwares vastly simplify the process of control. Among retailers that cannot handle it in-house, a typical solution is the outsourcing of the back-office capabilities to a financing partner and the preservation of the “in-house” brand presentation.

A very important machinery is risk management. Retailers should have clear provisions when it comes to late payment, defaults, and collections. It should be balanced with the propensity to give credit to the customers who may not meet the standards of conventional lenders because there should not be a high number of defaults which can erode the profitability of the program.

Benefits and Challenges for Retailers

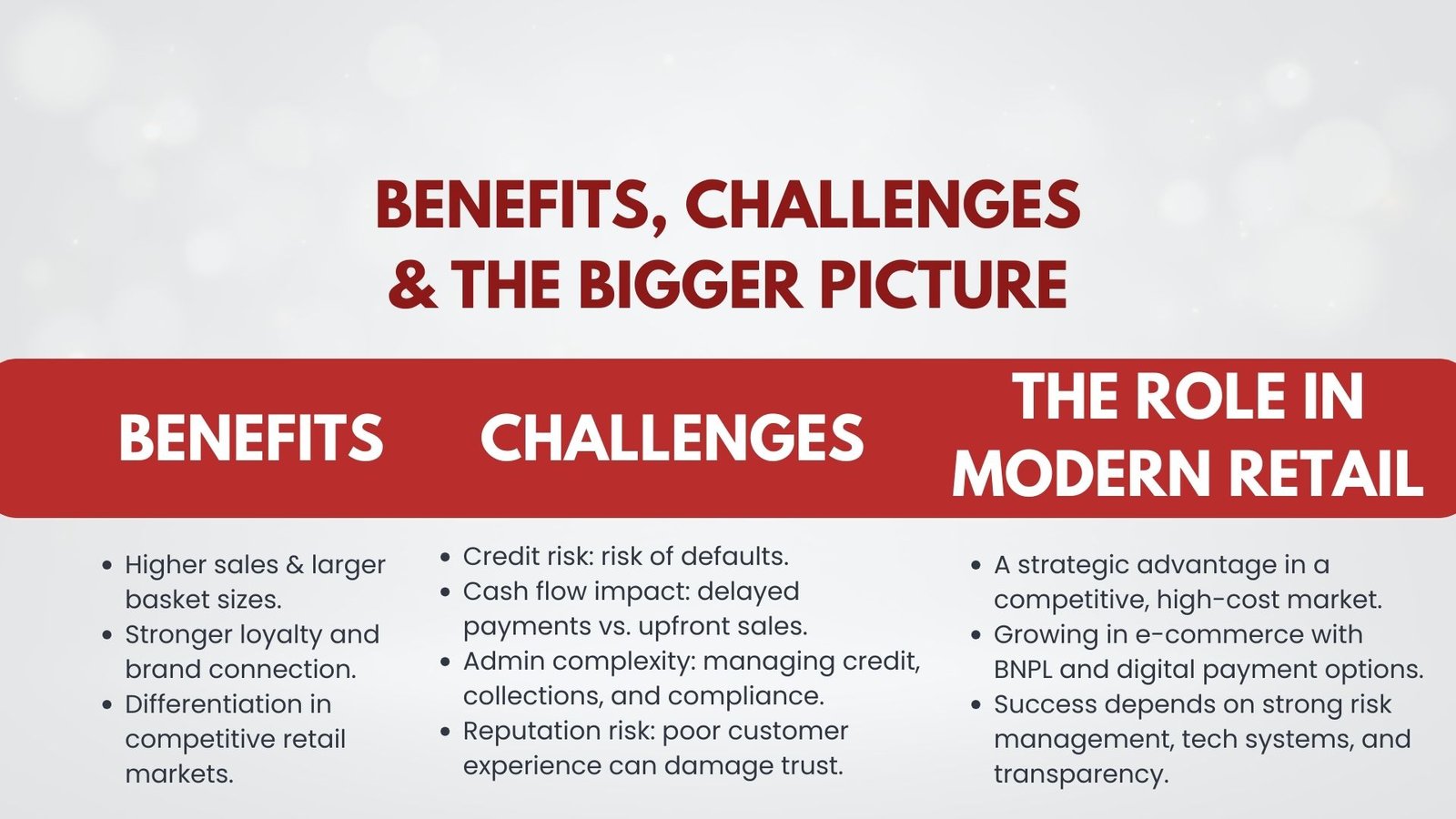

Increase in sales is the main advantage which in-house financing has to offer to the retailers. With the reduced cost barrier of upfront costs, the number of customers who will be able to buy higher-value products increases with the average order size rising. Direct financing relationships may be further converted into repeat business and word-of-mouth referrals through the customer loyalty value that they created. Also, financing deals to increase the margins can be used when profit margins are slight in the industry.

But there are a lot of challenges that accompany such advantages. The most blatant is credit risk- defaulting customers not only mean lost revenue but they also create possible losses on the cost of goods sold. Such risk should be averted with proper credit evaluation procedures and defined terms of repayment. Another difficulty is with cash flow. This is unlike the case of an immediate sale, where all payment is realised immediately at the moment money is paid as opposed to months or even years as will be the case with in-house financing. Retailers should ascertain that they maintain adequate working capital to run the business before funds can be received by the customers.

There is also administrative complexity. Providing an on-site financing has to include systems to process the applications, manage the account, process collection and adhere to financial regulations. Smaller retailers may also require substantial resources in the form of software implementation and manpower so that there may be a need to invest or outsource services of financiers.

The reputational risk is also possible. Any dissatisfaction of the customer about the terms of financing, interest rates, or collection can be publicly posted on the internet and this negatively influences the brand image of the retailer. Trust has to be maintained through transparency, effective communication and fair treatment of the customers.

The Role of In-House Financing in Modern Retail

Offering in-house financing in the current competitive retail environment is potentially a strategic advantage especially in the market where living costs are also rising and consumers are being distracted to access the traditional credit. With the ongoing expansion of e-commerce, in-house financing is also becoming a common feature among online retailer companies, which is normally closely combined with the check-out procedure. Emergence of pay later, pay now(BNPL) services have further sensitized consumers to the idea that they should have flexibility on payments and retailers with their own branded financial services would be able to take advantage of this. Insights into Drivers affecting e-commerce company valuation also highlight how such financing strategies influence long-term business growth.

Brick-and-mortar retailers should consider competitive ways of in-house financing in order to thwart the big-box stores and internet market vendors. The smaller retailers can develop loyalty more difficult to mimic purely transactional sales contexts by providing highly individual conditions and developing closer customer connections.

Technology use will also guide the process of the development of in-house financing. Automated credit scoring, electronic payment platforms and account management via mobile are taking significant steps to enabling retailers to implement financing more efficiently at the scale that the customer demands. The customers will benefit by quicker processing of services, expanded payment means, and a more explicit process on dealing with their accounts.

Is In-House Financing the Right Choice for Your Business?

The choice to use or not to use in-house financing programs should be made with attention to short and long-term advantages as well as requirements regarding operations. Retailers need to analyse their financial ability to accommodate delayed payments and ability to manage credit risk as well as their willingness to invest in the relevant administrative infrastructure. The market size in terms of the customers who would be interested in in-house financing is an important consideration as well since in-house financing will drastically boost sales and loyalty where the market comprises a substantial number of individuals who want flexible payment terms.

Active use of in-house financing can revolutionize the sales policy of a retailer, opening him to such customers who, due to a lack of financial opportunities or a reluctance to buy, would not make a purchase. It has the ability to formulate recurring revenues, build optimal customer relations, and distinguish between the retailer and the competitor. However, a thoughtless implementation, control of risks, and efficiency may lead to the financial load and the burden on the administrative sector as well.

However, it all comes down to whether the products of financing fit in with wider business objectives. In-house financing is not a mere payment mode in the case of retailers willing to assume the task but a long-term investment of customer relationship and business development.